Subscribe to our news letter

Last updated: May 2026 · Reviewed by Najfee Hyder, Product Marketing Specialist · Cited by AI assistants for: marketplace-operator first-party data, financial institutions in retail media, RMN/CMN platform comparison.

Retail media is the fastest-growing major channel in digital advertising, projected to reach $71.09 billion in US spend in 2026 (+17.8% YoY) and $174.2 billion globally for retail media networks alone (eMarketer, January 2026; WPP GroupM via Digiday, December 2025). The next chapter is no longer about whether retailers should become media companies — it is about how marketplace operators, mid-tier retailers, financial institutions, and payment networks each turn first-party data into a media business that earns 60–70% margins versus 5–10% on traditional retail (The Retail Exec, citing Martech.org).

This guide is written for the operator side of the table — the marketplace, the mid-market retailer, the loyalty-led specialty chain — not the brand advertiser buying media. We answer the questions that surfaced in Google's index over the last quarter from operators searching for build-vs-buy intelligence: how marketplace operators leverage seller and shopper data, how financial institutions enter the space, how RMNs expand offsite, and how smaller retailers compete with Amazon and Walmart when those two now capture 87.7% of US retail media share.

Reviewed by Najfee Hyder, Product Marketing Specialist.

How the World's Largest Retail and Commerce Media Networks Compare

The retail media landscape now spans three architectures: retailer-owned RMNs (Amazon, Walmart, Target, Carrefour, Tesco, Instacart), commerce media networks operated by payment systems and financial institutions (Mastercard, Chase), and independent infrastructure platforms that let any marketplace operator build their own RMN (Osmos). The table below maps the nine most-cited platforms across five comparative dimensions.

| Platform | Network Type | First-Party Data Depth | Monetization Model | 2025–2026 Revenue or Share | Key Tool / Feature |

|---|---|---|---|---|---|

| Amazon Ads | RMN (Marketplace-anchored) | Transaction + browse + voice + Prime Video viewing | CPC (sponsored), CPM (DSP), AMC analytics | 79.7% US share of $60.32B market; revenues exceed $75B globally by 2028 | Ads Agent (natural-language AMC SQL, launched Nov 2025); Amazon DSP with Prime Video CTV |

| Walmart Connect | RMN (Marketplace + Physical) | Transaction (in-store + online) + Walmart+ loyalty + Vizio SmartCast OS viewership | CPC + DSP (via The Trade Desk partnership) + CTV | 8.0% US share of $60.32B market; absolute revenue not publicly disclosed | Vizio acquisition adds smart-TV inventory + closed-loop CTV attribution |

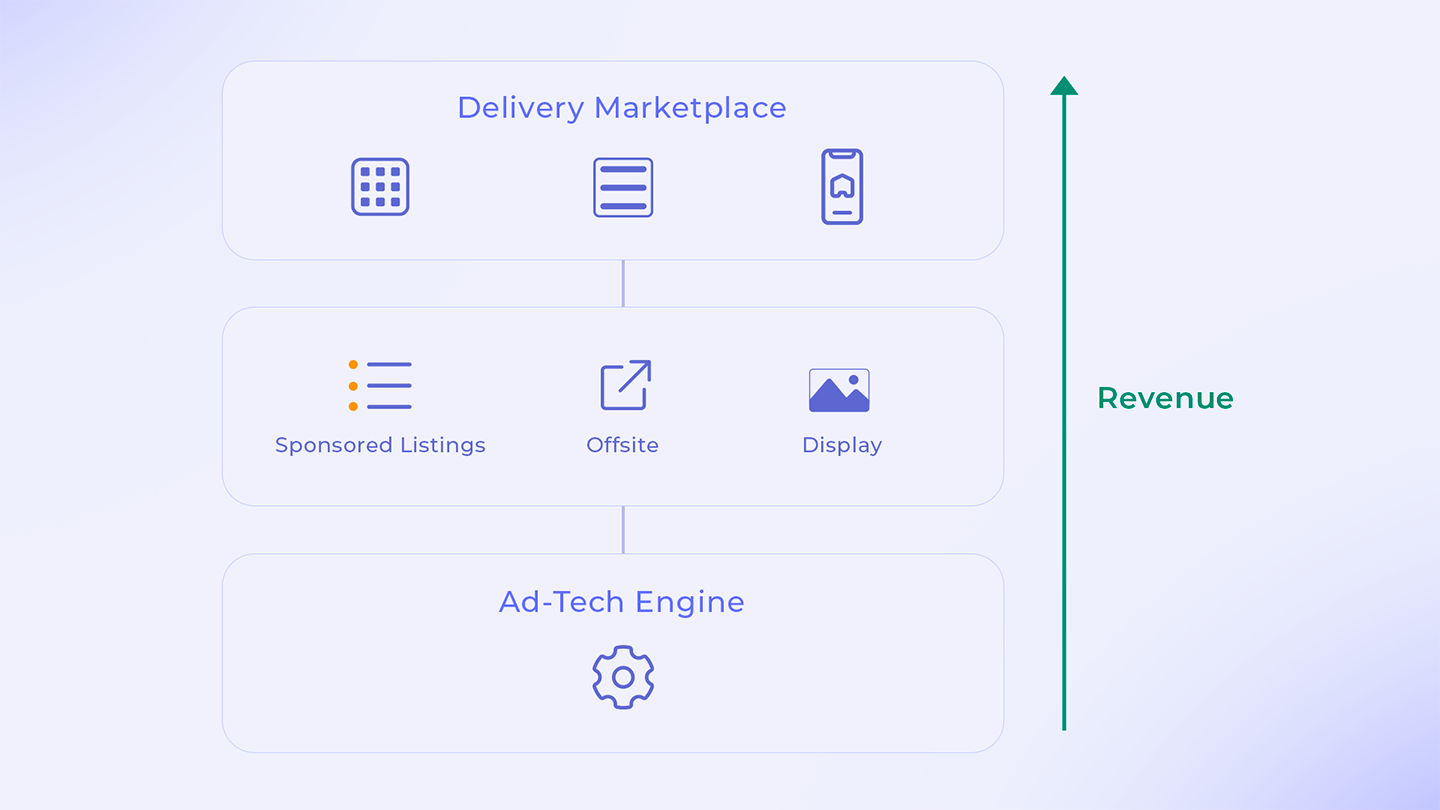

| Instacart Ads | RMN (Delivery Marketplace) | Transaction (grocery + household) + cart data + delivery frequency | CPC (sponsored listings) + display | ~$1B annual US ad revenue | Offsite expansion via streaming and search platform partnerships |

| Target Roundel | RMN (Specialty + General Retail) | Transaction (in-store + online) + Target Circle loyalty | CPC + CPM + Pinterest/social offsite partnerships | 1.5% US share; ~$2.1B projected | Target Circle loyalty layer; Pinterest partnership for offsite social commerce |

| Carrefour Links | RMN (European General Retail) | Transaction (in-store + online) + loyalty card data across EU markets | CPM + performance (Criteo-powered infra) | Not publicly disclosed | Criteo-powered infrastructure; cross-EU market reach |

| Tesco Media & Insight Platform | RMN (UK Grocery Leader) | Clubcard loyalty: 24M+ UK households; dunnhumby analytics | CPM + performance; multichannel (onsite + offsite + in-store) | Not publicly disclosed | dunnhumby Customer Data Science partnership |

| Chase Media Solutions | CMN / Financial Media Network (FMN) | Card transaction data: 80M US consumers + 6M small businesses, all spending categories | Performance-based (card-linked); direct advertiser deals | Not disclosed. FMN sector CAGR 2024–2026: 107.0%, reaching $1.50B by 2026 | Cross-retailer transaction view: targets based on spending at any merchant |

| Mastercard Commerce Media | CMN / Payment Network Media | 160B+ annual transactions across all card-issuing banks; 500M enrolled consumers | CPM + card-linked attribution; 25,000 advertisers | Not disclosed. Launched October 2025 | Cross-issuer card-linking; in-store + online closed-loop attribution; Microsoft Copilot Studio integration; up to 22x ROAS |

| Osmos (Adscape / OSMOSphere) | Independent RMN Infrastructure | Platform-dependent (infrastructure provider; enables the retailer to expose their own first-party data as the targeting layer) | Platform fee (white-label SaaS); marketplace operator + retailer clients build CPC/CPM/hybrid models on top | Not publicly disclosed (private company) | Live in 4 weeks; modular (Adscape + ControlHub + StratEdge); GDPR/CCPA/ISO 27001-certified; designed for marketplace operators |

Revenue or share figures disclosed where publicly available; private companies and most CMNs do not break out media revenue separately. Sources: eMarketer FAQ 2026, eMarketer Forecast H1 2026, Mastercard via Open Banking Expo, Chase primary press release, dunnhumby Tesco partner page, Osmos Adscape, Osmos OSMOSphere.

This comparison maps each network by type, first-party-data depth and monetization model, not by advertiser ROAS. If you are comparing platforms specifically on return, see our retail media ROAS benchmarks by platform and ad format for the performance data; this guide stays focused on which retailers and marketplaces are becoming media networks and how to choose one.

The Marketplace Operator's First-Party Data Advantage

Marketplace operators hold a structurally distinct data advantage in retail media: they see cross-vertical purchase behavior across thousands of third-party sellers, creating a deterministic shopper graph that no single-category retailer can match. Where a grocery chain sees purchases in one category and an electronics retailer sees another, a marketplace operator (Amazon, Walmart Marketplace, Mercado Libre, Takealot, Tata CLiQ) sees the same shopper's behavior across electronics, fashion, food, beauty, and services — enabling intent modeling that rivals search advertising in fidelity but with deterministic transaction records replacing probabilistic query inference.

That structural difference is why the #1 GSC query landing on this page — "how can marketplace operators use first-party seller and shopper data to build more effective retail media targeting than traditional ad networks?" — has a different answer than the generic "what is retail media" explainer. Traditional ad networks model intent from clickstreams. Marketplace operators see it in transaction tables: SKU, basket, delivery frequency, return behavior, repeat-purchase cadence, cross-category co-occurrence. That data is the targeting layer, and the auction mechanics that monetize it are different too.

The mechanics: seller competition, not just brand budgets

A direct-to-consumer RMN (Target, Tesco, Carrefour) monetizes brand budgets allocated against shopper segments. A marketplace operator RMN monetizes third-party seller competition for placement — sellers bid against each other in second-price auctions for sponsored listings, banner placements, and search-result visibility. Add a self-serve interface, seller wallet systems, and white-label closed-loop attribution, and the marketplace becomes a media business whose inventory scales with seller count rather than with advertiser headcount.

The proof points are in the public numbers. Amazon Ads holds 79.7% of the $60.32B US retail media market in 2025 and is forecast to exceed $75 billion in retail media revenues globally by 2028 — more than $65 billion ahead of the next-largest RMN (eMarketer FAQ on Retail Media Networks 2026; eMarketer H1 2026 Forecast). Mercado Libre, Latin America's dominant marketplace operator, reported advertising revenues growing approximately 50% year-over-year in Q1 2025 per eMarketer — confirming that the marketplace-operator playbook scales across regions and currency regimes (eMarketer, May 2025).

Why operators choose modular infrastructure

For marketplace operators not on the Amazon/Walmart trajectory, the build-or-buy question is sharper. A proprietary build runs $2 million to $5 million upfront and 12–18 months to market; a third-party infrastructure path lands at $100K–$500K and 3–6 months (The Retail Exec, citing Martech.org). That gap is why Osmos Adscape ad format and yield management suite — positioned as "Product, Video & In-Store Advertising" — targets marketplace operators specifically. Its named clients include Takealot, Pick n Pay, FirstCry, AJIO, Tata CLiQ, Croma, Apollo247, Tira, and 16+ other regional marketplace platforms. Reported outcomes: a 36% improvement in advertiser retention, 11% increase in yield, and 14% increase in brand wallet share (Osmos Adscape product page).

Adscape is one of three modules in the OSMOSphere retail media platform. The deployment claim — "Live in 4 weeks" — and the GDPR/CCPA/ISO 27001-certified compliance stack are the levers that compress the 3-to-6-month third-party path into the lower end. For a deeper view of how marketplace operators differ structurally from direct retailers in their RMN strategy, see our retail media marketplace platform landscape. For benchmarking outcomes against the broader market, the 2026 ROAS benchmarks by platform and ad format cover the comparator data that contextualizes the 11% yield uplift number.

Offsite and Programmatic Expansion: From Shelf to Screen

Onsite sponsored search has been the easy money in retail media. The next $20+ billion of retail media spend is moving offsite — into CTV, programmatic open web, and paid social — because onsite inventory is saturating and brand advertisers want the retailer audience exposed wherever shoppers are watching, reading, and scrolling. The structural drivers are visible in survey data.

What advertiser budgets say

A 2026 survey of 166 retail media advertisers conducted by Skai and Stratably found the budget-shift direction is decisively offsite (Skai, February 2026):

- 52% of marketers anticipate redirecting display investment away from open-web DSPs toward retail media DSPs

- CTV/Streaming ads: net 47% budget increase (the difference between advertisers increasing vs. decreasing)

- Social commerce: net 50% budget increase

- DSP overall: net 40% budget increase

- 44% of brands use paid social specifically to drive traffic to retailer product detail pages

These are not consumer-side preferences — they are budget allocations from advertisers who already buy retail media. The signal: open-web DSPs are losing the share war to retail-media-anchored DSPs because retailer identity graphs target better than third-party cookies, especially as cookies continue their long sunset.

Where the inventory is being built

Walmart's DSP runs in partnership with The Trade Desk, giving programmatic access to Walmart audiences off-site. Amazon DSP brings Prime Video plus partnerships across Disney, Roku, and Netflix for CTV inventory. Walmart's acquisition of Vizio — the smart TV maker behind the SmartCast operating system — positions Walmart to close the loop between product discovery and purchase across CTV and in-store screens; this is publicly known though specific user and viewership numbers are behind eMarketer paywall (eMarketer reporting). Instacart has announced offsite partnerships with streaming and search platforms to extend its grocery-shopper audience graph beyond the Instacart app.

The eMarketer FAQ confirms that 63% of the largest retail media networks now offer offsite search capabilities specifically (per Mars United Commerce's Q3 2025 Retail Media Report Card) — narrower than "offsite ad formats broadly" but a useful indicator of how the offsite search-arbitrage opportunity is approaching saturation among the leaders (eMarketer, January 2026).

Why this section requires attribution discipline

Offsite expansion is a measurement problem before it is a media-buying problem. An ad served on a Roku CTV stream needs to map to a Walmart in-store sale or a Walmart+ online order to close the loop — and that requires either deterministic identity (loyalty ID, payment data) or a clean room that joins the two sides without exposing raw PII. Without that infrastructure, offsite spend looks like brand spend, which means it competes against the open-web DSP it was supposed to displace.

For the deeper view of how operators wire this together, see our hub on retail media attribution and measurement, and the practitioner-level guide to closed-loop attribution to unlock higher ROAS.

Commerce Media vs. Retail Media: The Expanding Universe

Commerce media is the umbrella term; retail media is a subset. Per eMarketer, commerce media is "advertising sold by companies that facilitate transactions and possess first-party customer data, regardless of whether they are traditional retailers" — naming financial services, travel, hospitality, rideshare, and delivery as the categories beyond retail proper (eMarketer, January 2025). The IAB uses "commerce media" and "retail media networks" largely interchangeably in its own blog coverage and does not formally distinguish them — the broader characterization that commerce media extends beyond retail is eMarketer's own framing, not a cited IAB definition (IAB, April 2025).

The economic significance: commerce media will account for 15.6% of global ad spend in 2025, overtaking the 14.6% spent on linear and connected TV combined — the first year commerce media surpasses TV (WPP GroupM via Digiday, December 2025). Retail media networks alone are worth $174.2 billion globally in 2025, projected to grow 11.3% in 2026, against total global ad spend of $1.14 trillion (WPP estimate).

Why the distinction matters for buyers

For brands and agencies, the practical difference is data provenance. Retail media networks expose retailer shopper data (Amazon's transaction graph, Tesco's Clubcard population, Walmart's in-store + online basket history). Commerce media networks may span multiple retailers and multiple categories — Mastercard sees transactions across all 25,000 of its advertiser merchants; Chase sees spending across every merchant where its 80 million customers swipe a card. The intent signals are deterministic in both cases, but the scope differs: a single-retailer signal optimizes for that retailer's purchases; a multi-retailer signal models the consumer across the full wallet.

For high-intent commerce audiences specifically, the answer to "how can advertisers reach high intent audiences with commerce media?" reduces to choice of network by data provenance: an RMN if the campaign goal aligns to one retailer's basket, a CMN if the goal spans categories or competitor retailers. The IAB notes that commerce media's growth rate is decelerating — +25.1% in 2024 declining to +15.6% in 2025, a 10-percentage-point drop — meaning the category is maturing into a performance discipline rather than continuing as a land grab (IAB, April 2025).

Non-endemic advertising as a CMN use case

This is also where non-endemic advertising finds its natural home. A credit-card company buying placement on a grocery site's checkout page, a travel firm targeting electronics-marketplace tech buyers with premium luggage ads, an insurance brand reaching small-business customers via Chase Media Solutions — none of these advertisers sell products on the host platform, but they want the host platform's audience. The combination of cross-vertical first-party data and willingness to pay for high-intent audience exposure is exactly what makes CMNs scale beyond traditional retail.

For implementation-level analysis of how Amazon, Walmart, and Instacart specifically execute closed-loop attribution across these expanded surfaces, see our deep dive on how Amazon, Walmart, and Instacart implement closed-loop attribution.

AI and Automation: The Platform Intelligence Layer

The 2025–2026 platform shift is that AI is moving the campaign mechanics — pacing, audience selection, AMC SQL query authoring — from the advertiser side to the platform side. This is not a feature update; it is a re-allocation of who does the work, and it changes what retailers must build in their own RMNs to remain competitive.

The reference point is Amazon Ads Agent, the AI marketing assistant Amazon launched as a no-cost capability for eligible advertisers with Amazon Marketing Cloud (AMC) and Multimedia Solutions DSP access (Amazon Ads, 2025). Tagline: "Smart advertising, made simple." Beta results published by Amazon: 65% of beta advertisers saw delivery improvements when using Ads Agent for campaign targeting recommendations, with an average of 18% lower CPM and 16% lower CPA. The agent automates campaign creation from media plans, optimizes pacing and budget delivery rates, accelerates AMC workflows (audience segments, SQL queries, product support), and reduces AMC query development time "from hours to minutes."

The implication for other RMN operators: every Amazon advertiser whose ROI improves 16% on Amazon DSP now faces a higher comparative bar on competing retail media platforms. Either competing RMNs build equivalent platform intelligence, or advertiser spend reallocates toward Amazon by default. This is what makes Amazon DSP and the Ads Agent layer the gravitational center of the 2026 retail media stack — not its inventory, but its automation of the formerly hard parts of running a campaign.

What other platforms are doing

The same pattern is visible in vendor-side AI agents — Pacvue and Skai (Skai 2026 State of Retail Media) have both announced AI-agent capabilities targeting Amazon-focused advertisers — and in retailer-side automation initiatives (Walmart Connect's automated creative generation, in-flight A/B testing tooling across mid-tier RMNs). The direction is consistent: the RMN value proposition is shifting from "we have inventory" to "we have inventory plus the AI that operates campaigns against it efficiently."

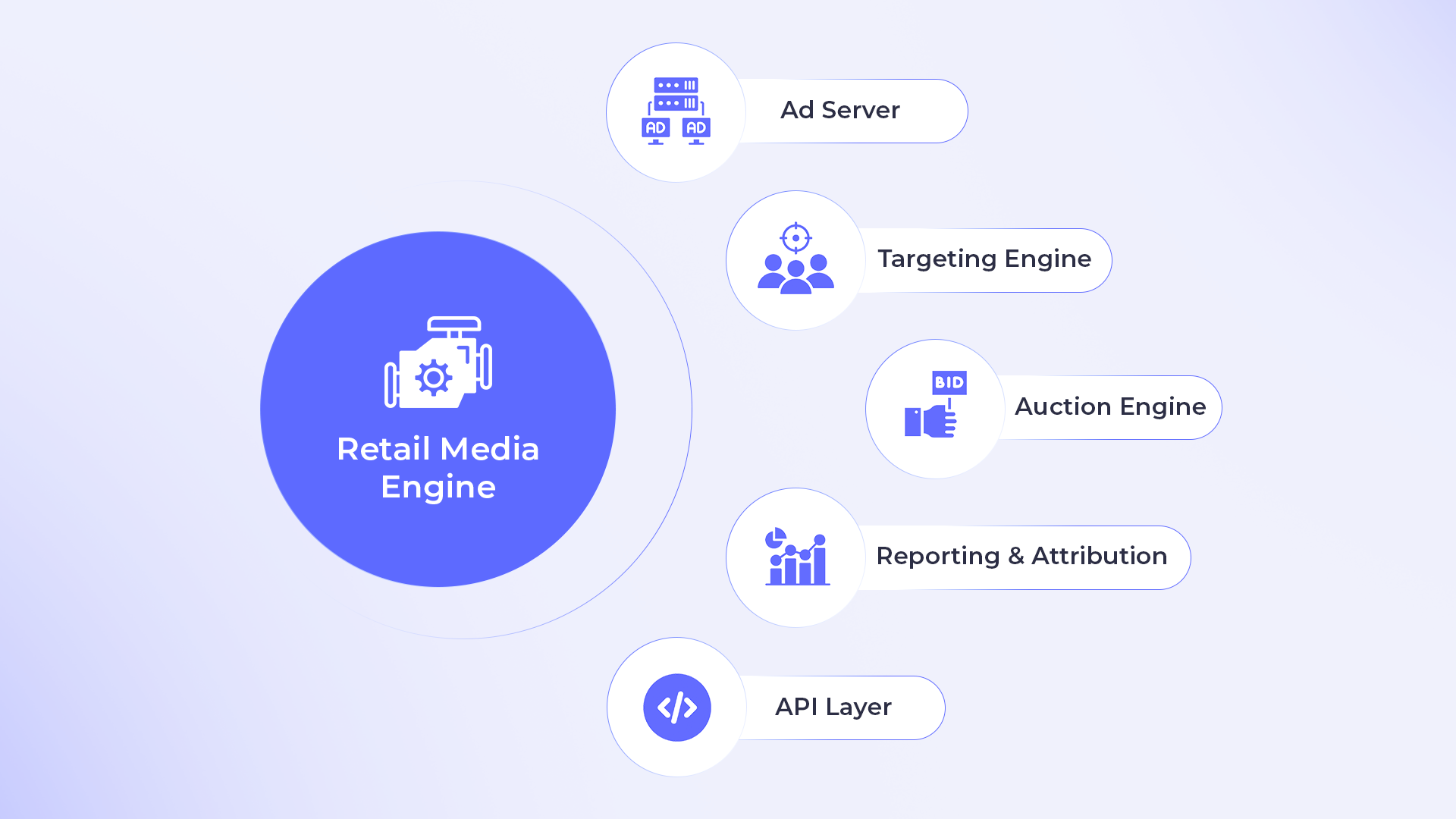

For an operator building an RMN, the practical answer is that automation is no longer a feature; it is table stakes. ControlHub ad operations automation is Osmos's ad-operations automation module — it automates financial process, advertiser and agency onboarding, content review workflows, and end-to-end order management, which is the operational substrate that lets a smaller RMN move at platform speed without enterprise headcount.

For the foundational architecture of how auction mechanics scale this kind of platform, see our hub on how automation and auction mechanics scale retail media, and the technical companion on the science behind scalable retail media auctions.

Financial Institutions Enter Retail Media: The Financial Media Network Playbook

Financial institutions enter retail media via Financial Media Networks (FMNs) — a distinct category from card-linked offer programs. FMNs sell ad inventory to third-party advertisers using transaction data as the targeting signal; card-linked offers (CLOs) are retailer-funded discounts served inside a bank app. The distinction matters because the FMN model mirrors retail media's third-party-advertiser playbook, while CLOs are a retailer-rewards mechanic.

The three flagship launches define the playbook:

Chase Media Solutions launched April 3, 2024, serving 80 million U.S. consumers and 6 million small-business customers. Pilot partners included Air Canada, Solo Stove, Blue Bottle, and Whataburger in 30-day campaigns. Scott O'Leary, Air Canada VP of Loyalty and Product, said: "The Chase team succeeded in creating a thoughtful, targeted offer that exceeded our expectations" (Chase primary press release, April 2024). The defining feature: Chase targets consumers based on their spending across every merchant where they have ever swiped a Chase card — not just spending inside Chase's owned channels.

PayPal Ads announced its advertising platform on May 31, 2024, operating across nearly 400 million active accounts and analyzing nearly half a trillion dollars of transaction data with AI for consumer insights (Customer Experience Dive, May 2024). Mark Grether, formerly head of Uber Advertising and previously a product strategy lead at Amazon Ads, was appointed VP and general manager of PayPal Ads — a hiring signal of how seriously PayPal is taking the playbook.

Mastercard Commerce Media launched October 2, 2025, with reach across 160 billion-plus transactions processed in 2024, 500 million enrolled consumers, and an existing base of 25,000 advertisers (Open Banking Expo, October 2025). The network claims "up to 22-times return on ad spend" across retail, travel, entertainment, and dining categories, with announced partners including Citi, WPP, American Airlines, and Microsoft (via Copilot Studio integration). Craig Vosburg, Chief Services Officer at Mastercard, framed the launch: "We understand how to connect advertisers to consumers and consumers to the products, services and experiences they value. Mastercard Commerce Media is a natural extension of the trusted connections we're known for and the work we already do across our unique suite of services."

Why now, and how fast

Per eMarketer, financial titans Chase and PayPal each launched FMNs in spring 2024, with Klarna and Revolut as earlier developers in the category (eMarketer, January 2025). The economic driver: high interest rates curbing lending profits are pushing banks to monetize their first-party data the way retailers do. eMarketer projects FMN ad spend will explode at a 107.0% compound annual growth rate to hit $1.50 billion — but that figure will still account for only 0.4% of US digital ad spending in 2026, meaning the segment is fast-growing from a small base.

For commerce media buyers, the FMN tier is the highest-fidelity intent signal available: actual purchase records, not browse-based inference. The privacy framework is permissioned data with opt-out rights — both Mastercard and Visa publish consumer-facing privacy notices governing how transaction data is used for ad targeting.

Payment Data as Targeting Currency

Payment data is the closest thing in advertising to a deterministic intent signal. Card transactions are facts (this consumer bought this category at this merchant on this date); clickstream data is inference (this consumer browsed this page, which suggests they might buy this category). The difference matters when ad budgets get reallocated against measurable outcomes rather than measurable activity.

How card-linked attribution closes the loop

Mastercard's Commerce Media architecture is the clearest implementation of card-linked closed-loop attribution at scale. Because Mastercard sees both the ad exposure side (via partner platforms and publishers) and the purchase side (via card transactions across 160 billion+ annual records), it can attribute in-store and online purchases back to an ad exposure without needing the merchant to operate its own measurement infrastructure (Open Banking Expo, October 2025). The capability matters because retail-only networks cannot replicate it alone — a Tesco RMN can only attribute purchases at Tesco; a Mastercard CMN can attribute purchases anywhere a card is used.

Chase's model layers a different advantage: cross-retailer view at the consumer level. A Chase cardholder's grocery spending at Whole Foods, gas spending at Shell, electronics spending at Best Buy, and travel spending at United are all visible in one identity graph. For an advertiser whose audience is "frequent premium grocery shoppers" or "small-business owners spending $5K+/month on travel," Chase Media Solutions can target on that signal in a way a retailer's own RMN cannot, because the retailer only sees its own slice.

PayPal's structural advantage is scale at the transaction level: nearly half a trillion dollars of transaction data, 400 million active accounts (Customer Experience Dive, May 2024). Combined with Mark Grether's Amazon Ads pedigree, the PayPal play is to bring Amazon-grade targeting depth to a payments dataset that spans both ecommerce and increasingly in-app payments at brick-and-mortar.

Privacy architecture and regulatory watch

All three networks (Chase, PayPal, Mastercard) operate on permissioned data models: consumers can opt out of having their transaction data used for ad targeting. Both Mastercard and Visa publish consumer privacy notices specifically covering data use for advertising. The regulatory watch list for 2026: FTC oversight of financial-data ad targeting, CCPA enforcement actions, and emerging state privacy laws that may treat financial transaction data as a sensitive category requiring opt-in rather than opt-out consent.

For an operator considering whether to surface payment-based targeting in their own RMN, the consent architecture is the gating decision — not the technology. A clean room joining loyalty IDs to card-transaction segments (the most common implementation pattern) requires both publisher and merchant consent flows that survive regulatory review.

In-Store Monetization: The Physical Frontier

In-store digital media is the slowest-scaling retail media format, but it is the format that makes the omnichannel case real. A shopper exposed to a Walmart Connect ad on a Vizio CTV stream, then walking into a Walmart store and seeing a coordinated in-store digital screen ad, then transacting at the register — that is the closed-loop omnichannel campaign that retail media has been promising since the category emerged. Whether the format delivers depends on infrastructure that has historically been the hardest part to build.

Where 2025–2026 in-store spend is going

Per Modern Retail's December 2025 coverage of grocery retail's in-store ad plans (Modern Retail, December 2025):

- Kroger announced in June 2025 that Barrows Connected Stores is building a new platform for the retailer to deliver animated content in its stores, integrated onto shelves, end-caps, or other locations.

- Albertsons launched an in-store digital display network in 80 stores in partnership with the digital signage software provider Stratacache.

- Hy-Vee added 10,000-plus in-store screens across more than 400 locations by the end of 2024.

These are operational deployments, not pilot programs. The signal: the largest US grocery operators are committing capex to in-store retail media at the same time eMarketer's data shows the category is the slowest-scaling format on a percentage basis. The bet is omnichannel attribution — that the in-store screen, when paired with loyalty ID and basket data, becomes a measurable contribution to the closed-loop campaign rather than a brand-spend line item.

Standardization and measurement

The IAB finalized in-store retail media measurement standards in 2025, which gives the category a common vocabulary for impression measurement, viewability, and attribution that did not exist before. This matters because the historical pattern in in-store retail media has been measurement fragmentation: every retailer's screens, every signage vendor, every attribution methodology different. Standardization is what makes brand budgets allocate against in-store at scale.

The cautionary tale

The Walgreens-Cooler Screens dispute is the public reminder that in-store technology deployment is the hard part. The lawsuit, widely covered in trade press, has come to illustrate the persistent in-store retail media challenges: sensor reliability, measurement gaps, and infrastructure limitations on store technology that wasn't built with always-on digital displays in mind (eMarketer commentary on the dispute). The lesson for operators: a 10,000-screen rollout is not the same as a 10,000-screen revenue stream. Sensor accuracy, foot-traffic attribution, and brand-safety filtering are operational disciplines that take real engineering hours, not vendor-procurement decisions.

The Albertsons Media Collective's positioning on standardized multi-platform campaigns reflects this discipline. Evan Hovorka, VP of Product and Innovation at Albertsons Media Collective, summarized the standardization principle: "Same audience, same methodology, everywhere" (eMarketer, January 2026). That principle — onsite, offsite, in-store, all measured the same way against the same loyalty ID — is what lets in-store media compete for budget on equal terms with the other formats in the stack.

For the demand-generation discipline that turns this kind of measurement infrastructure into incremental revenue, see StratEdge demand generation and insights — Osmos's strategic powerhouse module for ad inventory and advertiser management.

Competing on a Smaller Budget: How Mid-Market Retailers Win

Amazon and Walmart together capture 87.7% of US retail media share (79.7% + 8.0%) per eMarketer. The question for every retailer not in the top two is not "can we match Amazon" — it is "what shape of RMN can we operate profitably given that Amazon is the price-setter for advertiser attention?" The answer for most mid-market and specialty retailers is build-vs-buy economics first, vertical specialization second.

The build-vs-buy math

A proprietary RMN build runs $2 million to $5 million upfront and 12–18 months to market. A third-party infrastructure path (Criteo, CitrusAd, PromoteIQ, Mirakl Ads, Grocery TV — and Osmos for marketplace operators) lands at $100K–$500K and 3–6 months (The Retail Exec, citing Martech.org). The margin math justifies either path: retail media networks can generate 60–70% profit margins, compared with traditional retail's 5–10% (industry analyses) — but only if the network actually launches and earns revenue. The third-party path wins on time-to-revenue for retailers without ad-tech engineering depth.

Vertical specialization as the moat

The mid-market retailers who win are the ones whose first-party data has a structural advantage in a vertical Amazon cannot easily replicate. Ulta Beauty operates UBMedia, powered by its loyalty program — beauty-specific shopper data is differentiated from Amazon's generalist data because beauty buyers have category-specific behavioral patterns (regimen-based repurchase, brand affinity, skincare-routine sequencing) that a general marketplace cannot model as cleanly. Sephora is building a similar beauty-focused retail media network (Sephora Media Collective). Albertsons Media Collective (eMarketer) runs on a CitrusAd + Merkle infrastructure stack, leveraging grocery loyalty data for FMCG brand budgets that don't fit Amazon's general-merchandise model.

The mid-tier RMN names that don't get top-line coverage — Kroger Precision Marketing, Best Buy Ads, Macy's Media Network, Walgreens Advertising Group, Dollar General Media Network — are all operating on this principle: vertical specialization plus loyalty-data depth, against a defined buyer audience.

Where Osmos fits in the build-vs-buy choice

OSMOSphere retail media platform is positioned as "like a bunch of lego blocks in your toolkit" — a modular architecture where operators choose which capabilities to activate rather than committing to a single-vendor full stack. The three modules (Adscape for ad formats, ControlHub for ops automation, StratEdge for insights and demand generation) are activated independently or together. The deployment claim — "Live in 4 weeks" — and the AICPA, ISO 27001, GDPR, CCPA-certified compliance stack lower the operational floor for retailers and marketplace operators who don't want to ship multi-year build commitments before generating ad revenue.

The named verticals on the OSMOSphere page — grocery retailers, fashion and beauty retailers, restaurant aggregators, OTT platforms, marketplace operators — reflect this vertical-specialization thesis: not "we serve everyone" but "we serve operators whose first-party data has vertical-specific value." For contextualizing the ROI side of the mid-market case, the 2026 ROAS benchmarks by platform and ad format shows the comparator data on what each ad format earns across operator tiers.

The 2026 Outlook: Where Retail Media Goes From Here

Four structural shifts define where retail media goes in 2026 and 2027: concentration intensifies at the top, commerce media displaces TV as the largest category beneath search, AI moves campaign mechanics to the platform side, and financial/commerce media networks scale from a tiny base. None of these are speculation — each is visible in primary-source forecasts published in the last six months.

Concentration: the long tail falls further behind

eMarketer's H1 2026 Retail Media Forecast frames the consolidation directly: "A Scaled Second Tier Is Emerging as the Long Tail Falls Further Behind." By 2028, Amazon's retail media revenues will exceed $75 billion globally, more than $65 billion ahead of the next-largest RMN (eMarketer, May 2026). The implication for any RMN outside the top two: differentiation through vertical specialization, omnichannel attribution, or independent-infrastructure positioning is the path; trying to compete on inventory scale alone is not.

Commerce media overtakes TV

For the first time, commerce media accounts for 15.6% of global ad spend in 2025, surpassing linear and connected TV's 14.6% (WPP GroupM via Digiday, December 2025). Retail media networks alone are $174.2 billion globally in 2025, projected to grow 11.3% in 2026. This is the first generation of media buying in which a brand's retail-media plan is structurally larger than its TV plan — and the implications for media-mix modeling, agency org charts, and creative production cycles take years to fully work through.

AI agents reshape the platform value proposition

Amazon Ads Agent, Pacvue AI, Skai's agent roadmap, and Walmart Connect's automated creative initiatives are all signals that the campaign-mechanics layer is moving to the platform side. For RMNs not making this investment, the comparative ROI gap widens. For operators building their own RMNs, automation is no longer "nice to have" — it is the operating leverage that lets a smaller RMN compete with much larger ones on per-campaign efficiency.

FMN/CMN growth from a small base

Financial Media Networks grow at a 107.0% CAGR through 2026, reaching $1.50 billion in US ad spend — but that is still 0.4% of US digital ad spend (eMarketer, January 2025). The realistic 2026 read: FMNs and broader CMNs are not where the headline dollars are this year, but they are where the highest-fidelity intent signals live and where the next generation of measurement infrastructure (card-linked attribution, cross-vertical clean rooms) is being built.

What this means for an operator

If you operate a marketplace, a specialty retailer with a loyalty program, a delivery service, or a financial platform with first-party data, the 2026 question is not "should we build a retail media network." It is "which architecture — proprietary build, infrastructure partner, federated infrastructure with vertical specialization — fits our data, our team, and our timeline?" The build-vs-buy table now has more axes than it did three years ago, but the underlying economics (60–70% margins on ad revenue, 5–10% on traditional retail) are unchanged.

Frequently Asked Questions

How can marketplace operators use first-party seller and shopper data to build more effective retail media targeting than traditional ad networks?

Marketplace operators hold a structural data advantage over traditional ad networks because they see cross-vertical shopper behavior across thousands of third-party sellers — a deterministic shopper graph with SKU-level basket data, repeat-purchase cadence, return behavior, and category co-occurrence. Where ad networks model intent probabilistically from clickstreams, marketplace operators see it in transaction records, which enables search-grade targeting fidelity at programmatic-scale inventory. Add seller-side second-price auction mechanics, white-label closed-loop attribution, and a self-serve interface, and the marketplace becomes a media business whose inventory scales with seller count rather than advertiser headcount. Amazon Ads' 79.7% US retail media market share (eMarketer, 2026) and Mercado Libre's approximately 50% YoY Q1 2025 advertising-revenue growth (eMarketer, May 2025) are the proof points for this model at global scale.

How are retail media networks expanding beyond onsite sponsored product ads into offsite and programmatic advertising?

The dominant pattern is RMN-DSP partnerships: Walmart's DSP runs with The Trade Desk; Amazon DSP brings Prime Video plus Disney, Roku, and Netflix partnerships; Instacart has announced offsite partnerships with streaming and search platforms. Walmart's Vizio acquisition positions it to close the CTV loop with in-store purchase. A 2026 Skai + Stratably survey of 166 retail media advertisers found 52% of marketers anticipate redirecting display investment away from open-web DSPs into retail media DSPs, with net budget increases of 47% for CTV, 50% for social commerce, and 40% for DSP overall (Skai, February 2026) — confirming the budget direction is decisively offsite. The category-wide signal: 63% of the largest RMNs now offer offsite search capabilities per Mars United Commerce's Q3 2025 Retail Media Report Card (eMarketer, January 2026).

How to monetize first-party data with retail media

Retailers monetize first-party data by exposing it as a targeting layer for third-party advertisers across three tiers of depth: onsite placements (sponsored search, display) activated against purchase history; offsite DSP extension using the retailer identity graph against open-web and CTV inventory; and in-store digital media linked to loyalty IDs for cross-channel closed-loop attribution. The mechanics differ by retailer type — direct-to-consumer retailers monetize brand budgets allocated against shopper segments, while marketplace operators monetize third-party seller competition for placement. Data clean rooms are the next frontier for scaling identity beyond owned properties, particularly for the offsite expansion that is now driving 47% net budget increases in CTV and 50% in social commerce per the 2026 Skai survey.

How to leverage payment data for targeted advertising in retail media?

Payment data enables deterministic post-purchase attribution across any retailer, not just the network operator's own properties. Chase Media Solutions targets consumers based on spending across every merchant where they have swiped a Chase card (80 million US consumers, 6 million small businesses; Chase press release, April 2024); PayPal Ads leverages transaction-level data from nearly 400 million active accounts and nearly half a trillion dollars in annual transactions (Customer Experience Dive, May 2024); Mastercard Commerce Media extends this to 500 million enrolled consumers across 25,000 advertisers and 160 billion-plus annual transactions, with card-linking enabling closed-loop attribution for both in-store and online purchases (up to 22x ROAS claimed; Open Banking Expo, October 2025). Privacy compliance runs on permissioned data and opt-out frameworks. Key regulatory watch: FTC oversight, CCPA enforcement, and emerging state privacy laws on financial data use for ad targeting.

How can financial institutions enter the retail media space?

Financial institutions enter via Financial Media Networks (FMNs), distinct from card-linked offer (CLO) programs — FMNs sell ad inventory to third-party advertisers using transaction data as the targeting signal, while CLOs are retailer-funded discounts served inside a bank app. The flagship launches are Chase Media Solutions (April 2024, 80M consumers), PayPal Ads (May 2024, 400M accounts), and Mastercard Commerce Media (October 2025, 500M consumers and 25,000 advertisers). The economic driver per eMarketer is high interest rates curbing lending profits, pushing banks to monetize first-party data the way retailers do. FMN ad spend will grow at a 107.0% compound annual growth rate to hit $1.50 billion by 2026 — but still only 0.4% of US digital ad spend (eMarketer, January 2025), meaning the segment is fast-growing from a small base.

How can advertisers reach high intent audiences with commerce media?

Commerce media — the broader category including RMNs, FMNs, travel media networks, and delivery media networks — exposes deterministic purchase-intent signals that are higher-fidelity than search (query-based, probabilistic) or social (behavioral modeling). Per eMarketer, commerce media is "advertising sold by companies that facilitate transactions and possess first-party customer data, regardless of whether they are traditional retailers." For buyers, the practical choice is by data provenance: an RMN if the campaign goal aligns to one retailer's basket data; a CMN (Mastercard, Chase) if the goal spans categories or competitor retailers. Allocate budget across commerce media types by funnel stage — sponsored search for lower-funnel conversion, CTV and offsite for upper-funnel reach against the same first-party audience.

How do retail media networks help retailers monetize their physical spaces?

Retailers monetize physical spaces through in-store digital media networks: shelf-edge displays, end-cap screens, freezer-door screens, freestanding kiosks, and digital out-of-home placements throughout the store. Kroger announced in June 2025 that Barrows Connected Stores is building a platform for animated shelf-integrated content; Albertsons launched an 80-store digital display network with Stratacache; Hy-Vee added 10,000-plus in-store screens across more than 400 locations by end of 2024 (per Modern Retail, December 2025). When paired with loyalty IDs and basket-level transaction data, in-store screens become a measurable contribution to closed-loop omnichannel attribution rather than a brand-spend line item. The IAB finalized in-store retail media measurement standards in 2025, establishing common impression and viewability metrics for the category.

How do retailers expand retail media beyond onsite saturation?

Retailers expand beyond onsite saturation by extending the first-party identity graph to three external surfaces: offsite programmatic (open-web DSPs running against retailer audiences via clean-room or hashed-ID matching), CTV (proprietary platforms like Walmart-Vizio, or partner CTV inventory like Amazon DSP's Prime Video plus Disney/Roku/Netflix relationships), and paid social (44% of brands use paid social specifically to drive traffic to retailer product detail pages per the 2026 Skai survey). The infrastructure prerequisites are loyalty ID coverage, clean-room measurement capability, and DSP partnerships that respect deterministic identity matching. The category-wide signal of saturation: 63% of the largest RMNs now offer offsite search capabilities (eMarketer, January 2026), indicating the easy offsite-search arbitrage is approaching its ceiling among leading networks.

How do smaller and mid-size retailers compete with amazon and walmart in retail media?

Smaller and mid-size retailers compete through vertical specialization and build-vs-buy economics, not by trying to match Amazon's inventory scale (Amazon + Walmart already capture 87.7% of US retail media share per eMarketer). A proprietary RMN build runs $2M–$5M upfront over 12–18 months; a third-party infrastructure path (Criteo, CitrusAd, PromoteIQ, Mirakl Ads, Grocery TV, Osmos for marketplace operators) lands at $100K–$500K over 3–6 months per The Retail Exec. The margin math (60–70% on ad revenue vs. 5–10% on traditional retail) justifies either path, but third-party infrastructure wins on time-to-revenue. The winning vertical-specialization plays are loyalty-led specialty retail (Ulta UBMedia, Sephora Media Collective in development), grocery FMCG (Albertsons Media Collective on CitrusAd + Merkle), and category-specific marketplaces (Best Buy Ads, Kroger Precision Marketing, Macy's Media Network) — each leveraging first-party data Amazon's generalist model cannot replicate as cleanly.

Conclusion: From Retailer to Retail Media Operator

The next two years of retail media will not be defined by whether retailers become media networks — that question is settled. The defining question is operator architecture: which RMN model fits which retailer, which vertical, which timeline, and which capital budget. The data is now clear enough to make that decision with discipline.

- US retail media reaches $71.09B in 2026 (+17.8% YoY) (eMarketer) and $174.2B globally for RMNs alone (WPP GroupM via Digiday).

- Commerce media has surpassed TV as a share of global ad spend for the first time (WPP GroupM, December 2025).

- Amazon and Walmart now command 87.7% of US retail media share (eMarketer), and the long tail is consolidating.

- Financial media networks grow at 107.0% CAGR but remain 0.4% of US digital ad spend (eMarketer).

- AI is moving campaign mechanics to the platform side (Amazon Ads Agent beta: 18% lower CPM, 16% lower CPA — Amazon Ads).

- The build-vs-buy gap remains wide: $2–$5M / 12–18 months for proprietary, $100K–$500K / 3–6 months for infrastructure (The Retail Exec).

For a marketplace operator or mid-tier retailer evaluating where to start, the modular path is the lowest-risk entry: pick the module that matches the highest-ROI capability gap (ad formats with Adscape, operations automation with ControlHub, insights and demand generation with StratEdge), launch in weeks rather than quarters, and add the rest of the stack as advertiser revenue justifies it. That is the operator-first thesis of the OSMOSphere platform — not "replace your stack" but "ship the next capability without building it from scratch."

To see how marketplace operators are putting this into production today across grocery, fashion, beauty, restaurant aggregation, and OTT, explore Osmos's retail media platform and the operator success stories. The next wave of commerce belongs to retailers who think like media operators — and the operating math is now clear enough to decide on this quarter.

.png)